Staying on top of the crest of an industry is no easy task. It requires at least a highly qualified human resource team to discover growth opportunities ahead of the competition. Of course that additional political connections to enter those troubled geographies is as handy as a great load of industry nerds. Halliburton (HAL) seems to have both. The company has gone a long way since successfully tapping the first unconventional well using hydraulic fracturing 65 years ago. Today, fracking is a standard practice in the industry, but the firm has not stopped introducing new products and expanded across the globe. During the first quarter of 2014 alone, Halliburton has expanded its line of drilling optimization tools, introduced a new fracture diagnostic tool, a wireless controlled well testing solution and a line of fully integrated, custom-engineered service solutions. Is this why George Soros (Trades, Portfolio) continues to increase his holding in the company?

Market Trends and New Partnerships

Some news outlets have been the echo of Halliburton's decision to close its liberal facilities. The news remarked the fact that employees would be transferred to another location, but disappointment lingered as reminiscence of fracking golden years linger. "Halliburton is closing the facility as a result of changing business needs from its customers," according to Halliburton Senior Manager – PR & Community Initiatives Emily Mir. And that is the plain truth: The oil and gas industry is going through changes in North America with most companies beginning to focus on offshore drilling.

The offshore trend is so strong that it has the potential to revive companies believed to be permanently out of business, like Transocean (RIG) after the Deepwater Horizon incident. Hence, moving jobs from Liberal, Kansas, to Pampas, Texas, is coherent with current trends in North America as onshore reserves begin to dry. On the other hand, many offshore reserves remain untapped or undiscovered.

Halliburton has additionally looked for long growth opportunities abroad. For instance, the company opened its new Unconventional and Reservoir Productivity Technology Center at King Fahd University of Petroleum and Minerals, located in Dhahran Techno-Valley. Also, the firm announced the signing of a partnership agreement with Gubkin Russian State University of Oil and Gas for the development of unconventional resources in Russia, including the Bazhenov shale.

Prospects for an Industry Leader

Market positioning for Halliburton strength is evidenced by the fact that is a top three players in each of the product and service categories offered, and is present in all major hydrocarbon-producing regions of the world. Additionally, the firm enjoys very strong relationships with both private and state representatives. And prospects continue to improve as activities are driven away from onshore North American operations while no fleet unit is underutilized.

With respect to offshore activities, Halliburton's revenue in the segment is growing 25% faster than the industry average. However, management expects that leverage will decline as competition tightens. This issue is already being addressed by the firm through international opportunities. More specifically, new shale discoveries in Latin America are expected to help the company maintain an edge over the competition.

Additional trends that will keep Halliburton on top are a leading position in the North American oilfield services market, and market penetration in deepwater and underserved international regions. A third leg for the company's future profits aims at tripling mature field services revenue to $9 billion by 2016. And the key for all this to work is the dominant position developed in pressure pumping.

Currently trading at 24.9 times its trailing earnings, Halliburton's stock carries a 7% premium to the industry average. With stable net income through the last three years and increasing revenues amid legal battling and settlements, the company is in a great standing. So great that stock's face value has recovered from the blow suffered in 2011, a trend that gurus anticipated. That is why many bought the stock throughout 2013: Because it was a cheap entry price. Today, prospect investors are obligated to pay current prices or wait for another hard-to-come-by entry point.

Disclosure: Vanina Egea holds no position in any of the mentioned stocks.

About the author:Vanina EgeaA fundamental analyst at Lone Tree Analytics

Visit Vanina Egea's Website

| Currently 5.00/512345 Rating: 5.0/5 (1 vote) | Voters: |

Subscribe via Email

Subscribe RSS Comments Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

HAL STOCK PRICE CHART

59.46 (1y: +49%) $(function(){var seriesOptions=[],yAxisOptions=[],name='HAL',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1364792400000,39.93],[1364878800000,39.89],[1364965200000,38.75],[1365051600000,38.54],[1365138000000,38.6],[1365397200000,38.41],[1365483600000,39.11],[1365570000000,40.39],[1365656400000,41.17],[1365742800000,40.86],[1366002000000,38.66],[1366088400000,39.69],[1366174800000,37.69],[1366261200000,37.71],[1366347600000,37.21],[1366606800000,39.29],[1366693200000,39.69],[1366779600000,40.92],[1366866000000,40.75],[1366952400000,40.57],[1367211600000,41.57],[1367298000000,42.77],[1367384400000,42.08],[1367470800000,42.4],[1367557200000,42.55],[1367816400000,43.06],[1367902800000,43.42],[1367989200000,43.7],[1368075600000,43.56],[1368162000000,43.39],[1368421200000,43.56],[1368507600000,44.2],[1368594000000,44.13],[1368680400000,43.85],[1368766800000,45.25],[1369026000000,45.55],[1369112400000,44.83],[1369198800000,44.02],[1369285200000,43.52],[1369371600000,43.02],[1369717200000,43.37],[1369803600000,43.57],[1369890000000,42.63],[1369976400000,41.85],[1370235600000,42.39],[1370322000000,41.99],[1370408400000,41.76],[1370494800000,42.35],[1370581200000,43.16],[1370840400000,42.82],[1370926800000,42.04],[1371013200000,41.61],[1371099600000,43.08],[1371186000000,42.93],[1371445200000,43.62],[1371531600000,44.07],[1371618000000,43.05],[1371704400000,41.8],[1371790800000,41.79],[1372050000000,40.95],[1372136400000,41.15],[1372222800000,41.47],[1372309200000,41.84],[1372395600000,41.72],[1372654800000,42.45],[1372741200000,42.79],[1372827600000,42.65],[1373000400000,43.71],[1373259600000,43.92],[1373346000000,44.31],[1373432400000,44.13],[1373518800000,44.18],[1373605200000,44.64],[1373864400000,44.11],[1373950800000,43.63],[1374037200000,44.14],[1374123600000,44.74],[1374210000000,45.83],[1374469200000,45.08],[1374555600000,45.58],[1374642000000,44.82],[1374728400000,44.34],[1374814800000,45.98],[1375074000000,45.53],[1375160400000,45.23],[1375246800000,45.19],[1375333200000,46.41],! [1375419600000,46.3],[1375678800000,46.05],[1375765200000,45.85],[1375851600000,45.53],[1375938000000,46.14],[1376024400000,46.03],[1376283600000,46.02],[1376370000000,46.58],[1376456400000,46.82],[1376542800000,46.68],[1376629200000,46.95],[1376888400000,46.65],[1376974800000,47.35],[1377061200000,46.98],[1377147600000,47.82],[1377234000000,48.71],[1377493200000,48.44],[1377579600000,48.13],[1377666000000,48.9],[1377752400000,48.54],[1377838800000,48],[1378184400000,48.3],[1378270800000,49.08],[1378357200000,49.77],[1378443600000,49.54],[1378702800000,50.26],[1378789200000,50.32],[1378875600000,50.19],[1378962000000,49.2],[1379048400000,49.69],[1379307600000,49.82],[1379394000000,49.67],[1379480400000,49.75],[1379566800000,49.54],[1379653200000,49.34],[1379912400000,48.39],[1379998800000,48.75],[1380085200000,48.88],[1380171600000,48.71],[1380258000000,48.39],[1380517200000,48.15],[1380603600000,48.6],[1380690000000,49.09],[1380776400000,48.4],[1380862800000,49.06],[1381122000000,49.02],[1381208400000,48.66],[1381294800000,48.56],[1381381200000,50],[1381467600000,50.67],[1381726800000,51.35],[1381813200000,51.16],[1381899600000,51.97],[1381986000000,51.72],[1382072400000,52.47],[1382331600000,50.66],[1382418000000,51.78],[1382504400000,50.74],[1382590800000,51.1],[1382677200000,51.69],[1382936400000,52.03],[1383022800000,53.25],[1383109200000,53.26],[1383195600000,53.03],[1383282000000,53.23],[1383544800000,54.04],[1383631200000,53.13],[1383717600000,54.4],[1383804000000,53.9],[1383890400000,55.32],[1384149600000,55.3],[1384236000000,54.46],[1384322400000,55.54],[1384408800000,56.26],[1384495200000,56.23],[1384754400000,54.33],[1384840800000,53.76],[1384927200000,53.58],[1385013600000,54.2],[1385100000000,54.5],[1385359200000,52.7],[1385445600000,53.18],[1385532000000,52.42],[1385704800000,52.68],[1385964000000,52.01],[1386050400000,52.02],[1386136800000,50.62],[1386223200000,50.48],[1386309600000,50.56],[1386568800000,49.91],[1386655200000,49.43],[1386741600000,48.99],[1386828000000,49.59],[1386914400! 000,49.39! ],[1387173600000,50.13],[1387260000000,49.35],[1387346400000,49.91],[1387432800000,49.42],[1387519200000,50.54],[1387778400000,50.3],[1387864800000,50.68],[1388037600000,51.21],[1388124000000,51.08],[1388383200000,50.4],[1388469600000,50.75],[1388642400000,50.01],[1388728800000,50.13],[1388988000000,50.32],[1389074400000,50.2],[1389160800000,49.5],[1389247200000,49.61],[1389333600000,50.52],[1389592800000,49.58],[1389679200000,50.4],[1389765600000,50.64],[1389852000000,50.9],[1389938400000,50.66],[1390284000000,49.78],[1390370400000,50.54],[1390456800000,50.11],[1390543200000,48.61],[1390802400000,48.49],[1390888800000,48.33],[1390975200000,48.2],[1391061600000,49.44],[1391148000000,49.01],[1391407200000,48.33],[1391493600000,49.36],[1391580000000,49.27],[1391666400000,50.76],[1391752800000,51.97],[1392012000000,51.87],[1392098400000,53.84],[1392184800000,53.12],[1392271200000,53.46],[1392357600000,53.57],[1392703200000,54.13],[1392789600000,54.53],[1392876000000,55.38],[1392962400000,55.3],[1393221600000,56.37],[1393308000000,55.58],[1393394400000,55.16],[1393826400000,56.38],[1393912800000,56.9],[1393999200000,56.19],[1394085600000,56.92],[1394172000000,56.2],[1394427600000,56.47],[1394514000000,55.72],[1394600400000,55.39],[1394686800000,55.25],[1394773200000,55.19],[1395032400000,56.62],[1395118800000,56.9],[1395205200000,56.78],[1395291600000,57.36],[1395378000000,58.06],[1395637200000,57.78],[1395723600000,59.14],[1395810000000,58.37],[1395896400000,58.09],[1396011514000,58.09],[1396011514000,58.09],[1396018858000,59.46]]};var reporting=$('#reporting');Highcharts.setOptions({lang:{rangeSelectorZoom:""}});var chart=new Highcharts.StockChart({chart:{renderTo:'container_chart',marginRight:20,borderRadius:0,events:{load:function(){var chart=this,axis=chart.xAxis[0],buttons=chart.rangeSelector.buttons;function reset_all_buttons(){$.each(chart.rangeSelector.buttons,function(index,value){value.setState(0);});series=chart.get('HAL');series.remove();} buttons[0].on('click',function(e){chart.showLoading();reset_all_buttons();chart.rangeSelector.buttons[0].setState(2);var extremes=axis.getExtremes();$.getJSON('/modules/chart/price_chart_json.php?symbol=HAL&ser=1d',function(data){if(data!=null){var extremes=axis.getExtremes();axis.setExtremes(data[1][0][0],data[1][data[1].length-1][0]);chart.addSeries({name:'HAL',id:'HAL',color:'#4572A7',data:data[1]});if(data[0][1]>=0){display=data[0][0]+" (1D: +"+data[0][1]+"%)";reporting.html(display);}else{display=data[0][0]+" (1D: "+data[0][1]+"%)";reporting.html(display);} chart.hideLoading();}});});buttons[1].on('click',function(e){chart.showLoading();reset_all_buttons();chart.rangeSelector.buttons[1].setState(2);var extremes=axis.getExtremes();$.getJSON('/modules/chart/price_chart_json.php

Andrew Burton/Getty ImagesAnnette Bongiorno, Bernie Madoff's former secretary, leaves federal court Monday after being found guilty of charges of aiding, assisting and profiting from Madoff's Ponzi scheme. NEW YORK -- When it came down to it, the evidence was simply too overwhelming. That was what several jurors said Monday after they convicted five former Bernard Madoff associates of helping to conceal his multibillion-dollar Ponzi scheme. The verdict -- guilty on all counts -- came after just 20 hours of deliberations, which paled in comparison to the trial's extraordinary length. At more than five months, it was one of the longest white-collar criminal trials in the history of the federal court in Manhattan. But the jurors, interviewed after the verdict, said there was never really any doubt in their minds about the outcome. "It was the overall picture," said Sheila Amato, an art teacher from Rockland County, a suburb of New York City. "The facts speak for themselves." The five employees -- back-office director Daniel Bonventre, portfolio managers Annette Bongiorno and Joann Crupi and computer programmers Jerome O'Hara and George Perez -- claimed they believed Madoff's business was legitimate and were fooled into becoming unknowing accomplices. Starting in October, the jurors heard approximately 40 witnesses testify and saw thousands of documents admitted into evidence, creating a trial transcript that reached 12,000 pages. The closing arguments stretched nearly 25 hours over two weeks. In all, the jurors had to determine a verdict for 59 individual charges, with Bonventre alone facing 20 different counts of securities fraud, conspiracy, bank fraud, filing false tax returns, and falsifying records. Craig Parise, a fifth-grade teacher from Westchester County, another New York suburb, said the fact that the fraud persisted for so long made it hard to believe that the defendants, some of whom worked at the firm for decades, were completely unaware. "It would be different if it was a four-month Ponzi scheme," he said. "When it was 40 years, it's very hard to overlook that." Defense lawyers tried to undermine the government's star witness, Madoff's top deputy, Frank DiPascali, by painting him as a career con man with a talent for deception that rivaled only that of Madoff himself. But the jurors said they found his testimony credible and compelling. "It was pretty captivating," Amato said of DiPascali's testimony. "It wasn't scripted." That stood in contrast to the testimony from Bongiorno and Bonventre, who both made the unusual decision to take the stand in their own defense. The jurors emphatically rejected their claims that they had no idea what was going on. "I don't think it helped their case," Parise said. "It was slightly insulting. I think there was a lot of coaching going on." Another juror, Nancy Goldberg, an instructional assistant for at-risk students from Westchester, said the defense lawyers had done as well as they could without much ammunition. "They didn't have much to work with," she said. The trial's length forced some attrition in the jury box, with two jurors and two alternates excused because of illness or travel plans. After one juror was forced to leave in the middle of deliberations, the judge decided to move forward with only 11 members, a rare but not unheard of occurrence. Gloria Wynn, a church pastor from the Bronx, expressed relief that the grueling case had ended. "It was a long trial, and I'm glad it is over," she said. Goldberg, Amato and Parise, who all work in education, became close friends, commuting together on the train. Some of the jurors passed the time during lunch breaks by watching "The Chew," a cooking-themed talk show on ABC, in a jury lounge inside the courthouse. All the jurors exchanged phone numbers and email addresses, Parise said, and Goldberg suggested a reunion on Oct. 2.

Andrew Burton/Getty ImagesAnnette Bongiorno, Bernie Madoff's former secretary, leaves federal court Monday after being found guilty of charges of aiding, assisting and profiting from Madoff's Ponzi scheme. NEW YORK -- When it came down to it, the evidence was simply too overwhelming. That was what several jurors said Monday after they convicted five former Bernard Madoff associates of helping to conceal his multibillion-dollar Ponzi scheme. The verdict -- guilty on all counts -- came after just 20 hours of deliberations, which paled in comparison to the trial's extraordinary length. At more than five months, it was one of the longest white-collar criminal trials in the history of the federal court in Manhattan. But the jurors, interviewed after the verdict, said there was never really any doubt in their minds about the outcome. "It was the overall picture," said Sheila Amato, an art teacher from Rockland County, a suburb of New York City. "The facts speak for themselves." The five employees -- back-office director Daniel Bonventre, portfolio managers Annette Bongiorno and Joann Crupi and computer programmers Jerome O'Hara and George Perez -- claimed they believed Madoff's business was legitimate and were fooled into becoming unknowing accomplices. Starting in October, the jurors heard approximately 40 witnesses testify and saw thousands of documents admitted into evidence, creating a trial transcript that reached 12,000 pages. The closing arguments stretched nearly 25 hours over two weeks. In all, the jurors had to determine a verdict for 59 individual charges, with Bonventre alone facing 20 different counts of securities fraud, conspiracy, bank fraud, filing false tax returns, and falsifying records. Craig Parise, a fifth-grade teacher from Westchester County, another New York suburb, said the fact that the fraud persisted for so long made it hard to believe that the defendants, some of whom worked at the firm for decades, were completely unaware. "It would be different if it was a four-month Ponzi scheme," he said. "When it was 40 years, it's very hard to overlook that." Defense lawyers tried to undermine the government's star witness, Madoff's top deputy, Frank DiPascali, by painting him as a career con man with a talent for deception that rivaled only that of Madoff himself. But the jurors said they found his testimony credible and compelling. "It was pretty captivating," Amato said of DiPascali's testimony. "It wasn't scripted." That stood in contrast to the testimony from Bongiorno and Bonventre, who both made the unusual decision to take the stand in their own defense. The jurors emphatically rejected their claims that they had no idea what was going on. "I don't think it helped their case," Parise said. "It was slightly insulting. I think there was a lot of coaching going on." Another juror, Nancy Goldberg, an instructional assistant for at-risk students from Westchester, said the defense lawyers had done as well as they could without much ammunition. "They didn't have much to work with," she said. The trial's length forced some attrition in the jury box, with two jurors and two alternates excused because of illness or travel plans. After one juror was forced to leave in the middle of deliberations, the judge decided to move forward with only 11 members, a rare but not unheard of occurrence. Gloria Wynn, a church pastor from the Bronx, expressed relief that the grueling case had ended. "It was a long trial, and I'm glad it is over," she said. Goldberg, Amato and Parise, who all work in education, became close friends, commuting together on the train. Some of the jurors passed the time during lunch breaks by watching "The Chew," a cooking-themed talk show on ABC, in a jury lounge inside the courthouse. All the jurors exchanged phone numbers and email addresses, Parise said, and Goldberg suggested a reunion on Oct. 2. Popular Posts: 3 Game-Changing Tech Stocks to Put On Your Radar ScreenCandy Crush is Fun, But KING Investors Should Play ElsewhereNew Biotech Breakthrough: Buy Intermune Stock Recent Posts: New Biotech Breakthrough: Buy Intermune Stock Candy Crush is Fun, But KING Investors Should Play Elsewhere 3 Game-Changing Tech Stocks to Put On Your Radar Screen View All Posts

Popular Posts: 3 Game-Changing Tech Stocks to Put On Your Radar ScreenCandy Crush is Fun, But KING Investors Should Play ElsewhereNew Biotech Breakthrough: Buy Intermune Stock Recent Posts: New Biotech Breakthrough: Buy Intermune Stock Candy Crush is Fun, But KING Investors Should Play Elsewhere 3 Game-Changing Tech Stocks to Put On Your Radar Screen View All Posts

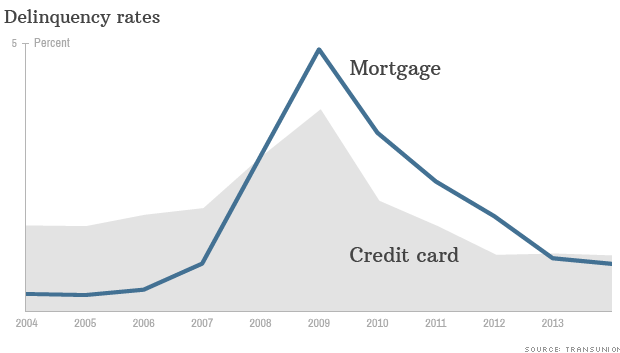

3 reasons to ignore the bad housing news

3 reasons to ignore the bad housing news