Bitcoin is a digital currency that exists almost wholly in the virtual realm, unlike physical currencies like dollars and euros. A growing number of proponents support its use as an alternative currency that can pay for goods and services much like conventional currencies. Bitcoin is the first and easily the most popular cryptocurrency, or currency that uses cryptography1 (see "Definitions and Key Concepts" at end of article) to control its creation, administration and security.

Bitcoin was set up in 2009 by a mysterious individual or group with the pseudonym Satoshi Nakamoto, whose true identity is yet to be revealed and who left the project in 2010. It rocketed to prominence in 2013, when the value of a Bitcoin soared more than 10-fold in a two-month period, from $22 in February to a record $266 in April. At its peak, based on more than 10 million bitcoins issued, the cryptocurrency boasted a market value of over $2 billion.

Bitcoin Versus Conventional Currencies

Bitcoin differs from conventional currencies in some very fundamental ways, as noted below (for the sake of simplicity, we use the U.S. dollar as a proxy for conventional currencies).

Bitcoin uses P2P technology without a central authority: Bitcoin is a decentralized currency managed by peer-to-peer technology (P2P2), without a central authority. All functions such as Bitcoin issuance, transaction processing and verification are carried out collectively by the network, without a central supervisor or agency to oversee operations. In contrast, a conventional currency is issued by a central bank as part of its mandate to manage national monetary policy. In the U.S., only the Federal Reserve has the power to issue dollars; it is also the central authority that conducts monetary policy, supervises banks, maintains financial system stability, and provides financial services to depository institutions.

Bitcoin is primarily digital: Although physical Bitcoins are available from companies such as Casascius and BitBills, Bitcoin has been designed primarily to be a digital currency. Physical Bitcoins are somewhat of a novelty, and the very idea of a tangible form defeats the purpose of a digital currency, according to the most ardent supporters of the concept. Conversely, your dollars exist primarily in physical form; the balances that you hold at your bank and online brokerage can be converted into physical dollars within minutes if you so desire.

Bitcoin has a maximum 21 million limit: The total number of Bitcoins that will be issued is capped at 21 million. The Bitcoin "mining"3 process presently creates 25 Bitcoins every 10 minutes (the number created will be halved every four years), so that limit will not be reached until the year 2140. While Bitcoin critics argue that the maximum limit is not large enough, supporters maintain that since each Bitcoin is divisible to eight decimal places, the number of fractional Bitcoins (called "satoshis") – at 21 x 1014 – will be more than enough for all conceivable applications. Conventional currencies, on the other hand, can be issued without limit.

Bitcoin is a complex product: The concepts of cryptocurrencies in general are abstruse and abstract, and understanding how and why Bitcoin works requires a fair degree of technological knowledge.

Bitcoin has limited acceptance: It has limited acceptance so far and cannot be used at brick-and-mortar storefronts, although that may eventually change if it continues to gain traction. The dollar, on the other hand, has near-universal acceptance as the world's global reserve currency.

Bitcoin transactions have limitations: A Bitcoin transaction can take as long as 10 minutes to confirm. Transactions are also irreversible and can only be refunded by the Bitcoin recipient. These limitations do not exist with conventional currencies, where debit and credit transactions are confirmed within seconds; certain transactions can also be reversed for valid reasons by the originator, without having to rely on the recipient's largesse.

Bitcoin balances are not insured: This means that if you lose your Bitcoins for any reason – for example, your hard drive crashes, or a hacker steals the digital wallet in which your Bitcoins are stored, or the Bitcoin exchange where you held a balance went out of business – you have little recourse. Currency balances held at banks, on the other hand, are insured against certain events such as bank failure by agencies like the Federal Deposit Insurance Corporation in the U.S.

How Bitcoin Works

Let's say you want to test the Bitcoin waters. The first thing you need to do as a new user is install a digital wallet on your computer or mobile device. This wallet is simply a free, open-source software program that will generate your first and subsequent Bitcoin addresses. There are three types of wallets – a software wallet (installed on your computer), a mobile wallet (which resides on your mobile device) or a Web wallet (located on the website of a service provider that hosts bitcoins).

Bitcoin uses public key encryption4 techniques for security. This means that when a new Bitcoin address is created, a cryptographic key pair consisting of a public key and private key – which are essentially unique, long strings of letters and numbers – is generated.

Each address has its own Bitcoins balance, so all you need to do is acquire a number of Bitcoins that will be held at one of the addresses in your wallet. You can acquire Bitcoins through a number of ways – by buying them from a Bitcoin currency exchange such as Mt. Gox or Bitstamp, or through a service like BitInstant that enables fund transfers between Bitcoin exchanges and supports various payment mechanisms.

Note that all Bitcoin transactions are stored publicly and permanently on the Bitcoin network, which means that the balance and transactions of any Bitcoin address are visible to anyone. Experts therefore recommend that Bitcoin owners create a new address for each transaction as a means of ensuring privacy and enhancing security.

Once you have created a Bitcoin address and have acquired Bitcoins, you can use them for an online transaction with a company that accepts Bitcoins as a payment mode. The company will send you the Bitcoin address to which you can send your Bitcoin payment. You direct the payment to that address; while the transaction takes place within seconds, verification can take 10 minutes or longer.

All Bitcoin transactions, without exception, are included in a shared public transaction log known as a "block chain". This is to confirm that the party spending the Bitcoins really owns them, and also to prevent fraud and double-spending.5

Why does transaction verification or confirmation take so long? Because the complex algorithms involved in Bitcoin mining (see description below) take time to solve, even with immense computing power at one's disposal.

An Example of a Bitcoin Transaction

Let's assume you want to make an online payment to a company – call it BitChamp – using 5 Bitcoins that you have in an address in your digital wallet. Here are the steps in the transaction:

BitChamp creates a new Bitcoin address and directs you to send your payment to it. This creates a private key (known only to BitChamp) and a public key (available to you and anyone else). Note that just as a seller does not need to know your physical identity if you pay cash, you do not need to disclose your real identity to BitChamp and can remain anonymous.

You instruct your Bitcoin client (the free Bitcoin software you first installed on your computer) to transfer 5 Bitcoins from your wallet to the BitChamp address. This is the transaction message.

Your Bitcoin client will electronically "sign" the transaction request with the private key of the address from where you are transferring the Bitcoins. Recall that your public key is available to anyone for signature verification.

Your transaction is broadcast to the Bitcoin network and will be verified in a few minutes. The 5 Bitcoins have been successfully transferred from your address to the BitChamp address.

Note that only the first two steps involve action by the seller and you respectively. The latter two steps are automatically executed by the Bitcoin client software and Bitcoin network. As well, storing the private key attached to an address safely and securely is of the utmost importance; otherwise, anyone who obtains the private key can control the Bitcoins at that address and use them fraudulently.

Bitcoin Pros and Cons

Bitcoin has a number of advantages:

As the first cryptocurrency to capture the public imagination, Bitcoin has "first mover" advantage and a head start over the competition.

Total issuance is limited to 21 million, so it is unlikely to be devalued because of the prospect of a massive influx of new bitcoins.

As a decentralized currency, Bitcoin is free from government interference and manipulation.

Transaction costs are much lower than with conventional currencies.

On the flip side, Bitcoin's disadvantages include:

The price of a Bitcoin has been increasingly volatile, making it difficult to assess its real value and increasing the risk of losses for investors in the cryptocurrency.

The relative anonymity of Bitcoin may encourage its use for illegal and illicit activities such as tax evasion, weapons procurement, gambling and circumvention of currency controls.

The fact that bitcoins exist primarily in digital form renders them vulnerable to loss.

Conclusion

Bitcoin has made significant progress in its adoption and usage since it was unveiled in 2009. Its evolution over the next few years will determine whether this leading cryptocurrency will become an integral part of the global financial system, or whether it is destined to remain a niche player.

Definitions and Key Concepts

1 Cryptography refers to the practice and technique of using encryption for secure communication and transmission of data and information.

2 In a P2P network, a group of computers is connected to enable the sharing of resources and information by users, and there is no central location for the network. This is diametrically opposed to a typical client-server network, where the central server controls the level of access by users to shared network resources. Popular applications of the P2P concept are Skype and file-sharing services such as BitTorrent.

3 Bitcoin mining refers to the computationally-intensive task of generating Bitcoins. While any computer can be put to the task of Bitcoin mining by using a free mining application, in reality a great deal of computing power is required to solve the extremely complex algorithms involved and to share those solutions with the entire Bitcoin network. The mining process is quite complicated and involves advanced concepts such as cryptographic hashes and nonces.

In simple terms, Bitcoin miners use powerful computers to track and compile pending Bitcoin transactions every 10 minutes into a new block. These miners then set to work doing the intensive number-crunching required to verify all the transactions in the block. This is a competitive process, and the first miner to solve the algorithms and verify the transactions transmits the results to the entire Bitcoin network. Upon confirmation by the rest of the network, the block is then added to the block chain. Each block includes a certain number of Bitcoins in a "coinbase" transaction that is paid out to the successful miner. This reward was set at 50 Bitcoins when the system first commenced operations in 2009, but was halved to 25 Bitcoins in November 2012, and will reduce by 50% approximately every four years.

4 Public key encryption combines a public key and a private key. While the public key is available to anyone, the matching private key is stored securely in the digital wallet and is generally password-protected. Each Bitcoin transaction is signed by the private key of the initiating user, providing mathematical proof that it has indeed originated from the owner of the address, and preventing the transaction from being altered once it has been issued. Since the key pair is mathematically related, any data or information encrypted with a private key may only be decrypted or deciphered with the corresponding public key and vice versa.

5 Double-spending means spending the same digital currency twice, something that is impossible with physical currencies.

Eric Nelson of Servo Wealth Management goes through the grim numbers in his July newsletter to clients.

Eric Nelson of Servo Wealth Management goes through the grim numbers in his July newsletter to clients.

Seth Wenig/APCEO Nick Woodman holds a GoPro camera in his mouth as he celebrates his GoPro's IPO. There were plenty of winners and losers this week, as the leading premium coffeehouse chain expanded its carbonated beverage offerings, and a disruptive video-streaming service got disrupted itself. Here's a rundown of the week's best and worst. GoPro (GPRO) -- Winner The initial public offering market got some fresh meat on Thursday when GoPro went public. The company behind the popular namesake cameras that extreme sports enthusiast like to wear was a hit. It priced at $24 a share -- at the high end of its initial range -- and that still wasn't enough. The stock opened at $28.65, closing out its first day of trading with a 31 percent gain. GoPro's growth has been stellar. Sales soared 87 percent last year to nearly hit $1 billion. However, there was a surprising decline in revenue during this year's first quarter. New GoPro investors are assuming that the most recent quarter's dip was a fluke. If it isn't a fluke, they can record their stumble in glorious high-def. Aereo -- Loser Sometimes it's the disruptor that gets disrupted. Aereo, the start-up service that offers local TV channels as a streaming platform, was pummeled by the U.S. Supreme Court. In a 6-3 decision, the court ruled that Aereo violated the copyrights of major TV networks by streaming their content without paying transmission fees. The move isn't the end for Aereo, but its prognosis has clearly deteriorated. Aereo thought that incorporating tiny remote antennas that subscribers can access online was similar enough to actual HD antenna ownership by individuals that its business model would be found to be legal. That didn't pan out, and consumers are unlikely to get a break this way from their ever-increasing cable and satellite TV bills. Starbucks (SBUX) -- Winner If you need to cool down in the Sun Belt, Starbucks has a few fizzy options. The java giant this week introduced its Fizzio line of carbonated beverages at 3,000 of its stores in the South. Fizzio is a line of handcrafted sodas that launched with three flavors (root beer, ginger ale and lemon ale), at 100 calories or less for 16 ounces. (Half as many calories as a Pepsi, and with cane sugar as the sweetener.) Starbucks is also letting customers pay 50 cents to have their iced teas and Refreshers beverages carbonated with the Fizzio machine. It's a smart call, giving non-coffee drinkers a new reason to walk into Starbucks. Steelcase (SCS) -- Loser Office furniture sales can be a good proxy by which to gauge the state of corporate America, but investors better hope that Steelcase is the exception.

Seth Wenig/APCEO Nick Woodman holds a GoPro camera in his mouth as he celebrates his GoPro's IPO. There were plenty of winners and losers this week, as the leading premium coffeehouse chain expanded its carbonated beverage offerings, and a disruptive video-streaming service got disrupted itself. Here's a rundown of the week's best and worst. GoPro (GPRO) -- Winner The initial public offering market got some fresh meat on Thursday when GoPro went public. The company behind the popular namesake cameras that extreme sports enthusiast like to wear was a hit. It priced at $24 a share -- at the high end of its initial range -- and that still wasn't enough. The stock opened at $28.65, closing out its first day of trading with a 31 percent gain. GoPro's growth has been stellar. Sales soared 87 percent last year to nearly hit $1 billion. However, there was a surprising decline in revenue during this year's first quarter. New GoPro investors are assuming that the most recent quarter's dip was a fluke. If it isn't a fluke, they can record their stumble in glorious high-def. Aereo -- Loser Sometimes it's the disruptor that gets disrupted. Aereo, the start-up service that offers local TV channels as a streaming platform, was pummeled by the U.S. Supreme Court. In a 6-3 decision, the court ruled that Aereo violated the copyrights of major TV networks by streaming their content without paying transmission fees. The move isn't the end for Aereo, but its prognosis has clearly deteriorated. Aereo thought that incorporating tiny remote antennas that subscribers can access online was similar enough to actual HD antenna ownership by individuals that its business model would be found to be legal. That didn't pan out, and consumers are unlikely to get a break this way from their ever-increasing cable and satellite TV bills. Starbucks (SBUX) -- Winner If you need to cool down in the Sun Belt, Starbucks has a few fizzy options. The java giant this week introduced its Fizzio line of carbonated beverages at 3,000 of its stores in the South. Fizzio is a line of handcrafted sodas that launched with three flavors (root beer, ginger ale and lemon ale), at 100 calories or less for 16 ounces. (Half as many calories as a Pepsi, and with cane sugar as the sweetener.) Starbucks is also letting customers pay 50 cents to have their iced teas and Refreshers beverages carbonated with the Fizzio machine. It's a smart call, giving non-coffee drinkers a new reason to walk into Starbucks. Steelcase (SCS) -- Loser Office furniture sales can be a good proxy by which to gauge the state of corporate America, but investors better hope that Steelcase is the exception.

In the latest of several reports indicating improvement, the European Commission recently said that its Economic Sentiment Indicator for the euro zone moved into positive territory this month for the first time in more than two years.

In the latest of several reports indicating improvement, the European Commission recently said that its Economic Sentiment Indicator for the euro zone moved into positive territory this month for the first time in more than two years.

Commercial space travel just a year away

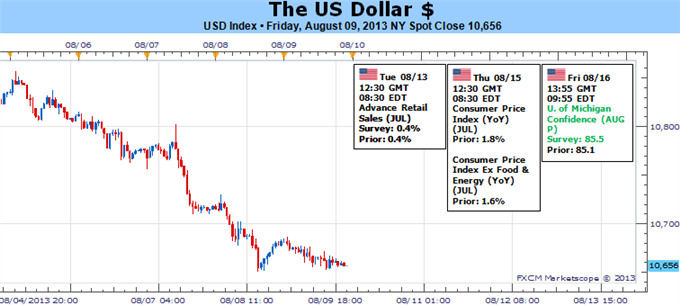

Commercial space travel just a year away  Dollar Could Put in for a Natural Rebound or Explosive RallyFundamental Forecast for US Dollar: BullishA range of Fed officials stay out of the way of the September Taper timetable US Treasury auctions show a slow rebound in foreign interest, but total demand weakening A strong showing in US service sector activity and trade reinforces growth, Taper outlook Over the past week, the Dow Jones FXCM Dollar Index (ticker = USDollar) suffered its worst weekly decline since December 2011 and its longest string of daily losses since December 2010. Taken without context, that is a strong bearish sign. However, when we consider the fundamental and technical backdrop; this situation looks like a launching point for a dollar rally. The question is whether it will be a mild, natural correction or an explosive rally with genuine trend generation. That outcome will be determined by the progress found on the market’s primary fundamental concerns: the market’s appetite for risk and speculation surrounding the Fed’s ‘Taper’.To understand where the dollar will move heading forward, we have to establish the conditions under which it has arrived at its current position. The slide through this past week was extraordinary for both its consistency and intensity. Yet, the slide evolved without the burden of the benchmark currency’s primary fundamental themes. Looking for evidence of a rebound in risk appetite; the speculative-favorite S&P 500 meandered – trading on the lowest non-holiday volume since the September 2011 terrorist attack – while other measures of sentiment similarly floundered. As for Taper premiums, both speeches by Fed officials’ speeches and data on the eco! nomic docket reinforced the probability of a September move by the central bank.Without conviction, the kind of move that we have seen this past week would more appropriately be labeled a ‘natural correction’. Though, traders know that such moves are temporary in nature without a strong shift in conviction and participation to change the underlying current. A simple look at market momentum, we find both the 100 and 200-day simple moving averages are below spot and rising steadily. So long as the systemic conditions behind the capital markets and investor sentiment don’t change, a return to trend for the greenback grows more likely with each day. Yet, the force of that transition depends on the accelerants available to facilitate it.The first thing we have to notice, is that the economic docket does not carry the kind of event risk that we would expect to definitively wipe out risk trends nor verify the September time frame for the Fed’s first reduction in its stimulus program. It is difficult to determine what known event risk short of the next FOMC rate decision (on September 18th) can carry enough influence to upset the current equilibrium. This past week, remarkably strong numbers for US trade and service-sector activity reinforced the more dubious – but positive – 2Q GDP and employment figures from the previous week. Furthermore, the Fed speeches from the period – particularly extreme dove Charles Evans – were clearly shaped to avoid contradicting expectations of a September start for the stimulus wind down. Yet, despite this combination, confidence in stimulus-backed speculative-position held fast. In the week ahead, we have another round of contributory data to the stimulus debate as well as central bank talks on tap; but these listings don’t seem to be any more convincing than what we have recently priced in. On Tuesday, non-voting Atlanta Fed President Dennis Lockhart (a hawk on QE) will speak on the economy, while voter St. Louis Fed Preside! nt James ! Bullard (a QE dove) is set to speak on monetary policy on Wednesday and the economy Thursday. For data, retail sales, the consumer price index and University of Michigan consumer sentiment survey are all notable.If this list of indicators and speeches can’t generate an explicit shift in risk trends, the natural ebb and flow will guide the dollar. Given the hefty move by the benchmark currency this past week despite the lack of drive, a rebound is likely. Yet, its potency and follow through will be questionable. Alternatively, should there be an innate shift in sentiment, the greenback can quickly return to its role as the market’s preferred reserve currency – for better or worse – and pitch into a serious trend.Looking at the backdrop for capital markets beyond S&P 500’s record highs, conditions looks highly suspect. This past week, volume on the S&P 500 was the lowest seen on a non-holiday period since the markets were closed after the September 2001 terrorist attacks in New York – an extension of a steady trend. Leverage used at the NYSE has moved to record highs. Exposure to exceptionally risky assets has grown. Retail interest in riskier assets has ramped up while ‘professional’ exposure has fled at the fastest pace in years. Meanwhile, volatility indicators show extreme complacency while rates of return are near record lows… - JKWritten by: John Kicklighter, Chief StrategistSign up for John’s email distribution list, here.original source

Dollar Could Put in for a Natural Rebound or Explosive RallyFundamental Forecast for US Dollar: BullishA range of Fed officials stay out of the way of the September Taper timetable US Treasury auctions show a slow rebound in foreign interest, but total demand weakening A strong showing in US service sector activity and trade reinforces growth, Taper outlook Over the past week, the Dow Jones FXCM Dollar Index (ticker = USDollar) suffered its worst weekly decline since December 2011 and its longest string of daily losses since December 2010. Taken without context, that is a strong bearish sign. However, when we consider the fundamental and technical backdrop; this situation looks like a launching point for a dollar rally. The question is whether it will be a mild, natural correction or an explosive rally with genuine trend generation. That outcome will be determined by the progress found on the market’s primary fundamental concerns: the market’s appetite for risk and speculation surrounding the Fed’s ‘Taper’.To understand where the dollar will move heading forward, we have to establish the conditions under which it has arrived at its current position. The slide through this past week was extraordinary for both its consistency and intensity. Yet, the slide evolved without the burden of the benchmark currency’s primary fundamental themes. Looking for evidence of a rebound in risk appetite; the speculative-favorite S&P 500 meandered – trading on the lowest non-holiday volume since the September 2011 terrorist attack – while other measures of sentiment similarly floundered. As for Taper premiums, both speeches by Fed officials’ speeches and data on the eco! nomic docket reinforced the probability of a September move by the central bank.Without conviction, the kind of move that we have seen this past week would more appropriately be labeled a ‘natural correction’. Though, traders know that such moves are temporary in nature without a strong shift in conviction and participation to change the underlying current. A simple look at market momentum, we find both the 100 and 200-day simple moving averages are below spot and rising steadily. So long as the systemic conditions behind the capital markets and investor sentiment don’t change, a return to trend for the greenback grows more likely with each day. Yet, the force of that transition depends on the accelerants available to facilitate it.The first thing we have to notice, is that the economic docket does not carry the kind of event risk that we would expect to definitively wipe out risk trends nor verify the September time frame for the Fed’s first reduction in its stimulus program. It is difficult to determine what known event risk short of the next FOMC rate decision (on September 18th) can carry enough influence to upset the current equilibrium. This past week, remarkably strong numbers for US trade and service-sector activity reinforced the more dubious – but positive – 2Q GDP and employment figures from the previous week. Furthermore, the Fed speeches from the period – particularly extreme dove Charles Evans – were clearly shaped to avoid contradicting expectations of a September start for the stimulus wind down. Yet, despite this combination, confidence in stimulus-backed speculative-position held fast. In the week ahead, we have another round of contributory data to the stimulus debate as well as central bank talks on tap; but these listings don’t seem to be any more convincing than what we have recently priced in. On Tuesday, non-voting Atlanta Fed President Dennis Lockhart (a hawk on QE) will speak on the economy, while voter St. Louis Fed Preside! nt James ! Bullard (a QE dove) is set to speak on monetary policy on Wednesday and the economy Thursday. For data, retail sales, the consumer price index and University of Michigan consumer sentiment survey are all notable.If this list of indicators and speeches can’t generate an explicit shift in risk trends, the natural ebb and flow will guide the dollar. Given the hefty move by the benchmark currency this past week despite the lack of drive, a rebound is likely. Yet, its potency and follow through will be questionable. Alternatively, should there be an innate shift in sentiment, the greenback can quickly return to its role as the market’s preferred reserve currency – for better or worse – and pitch into a serious trend.Looking at the backdrop for capital markets beyond S&P 500’s record highs, conditions looks highly suspect. This past week, volume on the S&P 500 was the lowest seen on a non-holiday period since the markets were closed after the September 2001 terrorist attacks in New York – an extension of a steady trend. Leverage used at the NYSE has moved to record highs. Exposure to exceptionally risky assets has grown. Retail interest in riskier assets has ramped up while ‘professional’ exposure has fled at the fastest pace in years. Meanwhile, volatility indicators show extreme complacency while rates of return are near record lows… - JKWritten by: John Kicklighter, Chief StrategistSign up for John’s email distribution list, here.original source