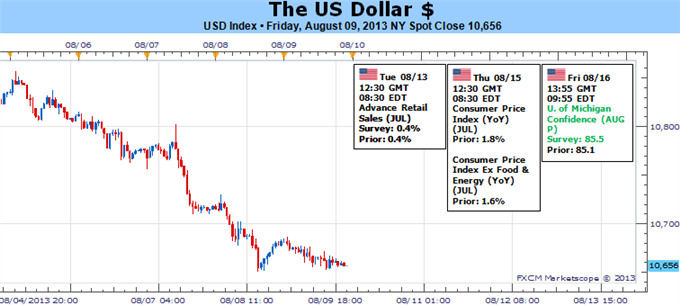

Dollar Could Put in for a Natural Rebound or Explosive RallyFundamental Forecast for US Dollar: BullishA range of Fed officials stay out of the way of the September Taper timetable US Treasury auctions show a slow rebound in foreign interest, but total demand weakening A strong showing in US service sector activity and trade reinforces growth, Taper outlook Over the past week, the Dow Jones FXCM Dollar Index (ticker = USDollar) suffered its worst weekly decline since December 2011 and its longest string of daily losses since December 2010. Taken without context, that is a strong bearish sign. However, when we consider the fundamental and technical backdrop; this situation looks like a launching point for a dollar rally. The question is whether it will be a mild, natural correction or an explosive rally with genuine trend generation. That outcome will be determined by the progress found on the market’s primary fundamental concerns: the market’s appetite for risk and speculation surrounding the Fed’s ‘Taper’.To understand where the dollar will move heading forward, we have to establish the conditions under which it has arrived at its current position. The slide through this past week was extraordinary for both its consistency and intensity. Yet, the slide evolved without the burden of the benchmark currency’s primary fundamental themes. Looking for evidence of a rebound in risk appetite; the speculative-favorite S&P 500 meandered – trading on the lowest non-holiday volume since the September 2011 terrorist attack – while other measures of sentiment similarly floundered. As for Taper premiums, both speeches by Fed officials’ speeches and data on the eco! nomic docket reinforced the probability of a September move by the central bank.Without conviction, the kind of move that we have seen this past week would more appropriately be labeled a ‘natural correction’. Though, traders know that such moves are temporary in nature without a strong shift in conviction and participation to change the underlying current. A simple look at market momentum, we find both the 100 and 200-day simple moving averages are below spot and rising steadily. So long as the systemic conditions behind the capital markets and investor sentiment don’t change, a return to trend for the greenback grows more likely with each day. Yet, the force of that transition depends on the accelerants available to facilitate it.The first thing we have to notice, is that the economic docket does not carry the kind of event risk that we would expect to definitively wipe out risk trends nor verify the September time frame for the Fed’s first reduction in its stimulus program. It is difficult to determine what known event risk short of the next FOMC rate decision (on September 18th) can carry enough influence to upset the current equilibrium. This past week, remarkably strong numbers for US trade and service-sector activity reinforced the more dubious – but positive – 2Q GDP and employment figures from the previous week. Furthermore, the Fed speeches from the period – particularly extreme dove Charles Evans – were clearly shaped to avoid contradicting expectations of a September start for the stimulus wind down. Yet, despite this combination, confidence in stimulus-backed speculative-position held fast. In the week ahead, we have another round of contributory data to the stimulus debate as well as central bank talks on tap; but these listings don’t seem to be any more convincing than what we have recently priced in. On Tuesday, non-voting Atlanta Fed President Dennis Lockhart (a hawk on QE) will speak on the economy, while voter St. Louis Fed Preside! nt James ! Bullard (a QE dove) is set to speak on monetary policy on Wednesday and the economy Thursday. For data, retail sales, the consumer price index and University of Michigan consumer sentiment survey are all notable.If this list of indicators and speeches can’t generate an explicit shift in risk trends, the natural ebb and flow will guide the dollar. Given the hefty move by the benchmark currency this past week despite the lack of drive, a rebound is likely. Yet, its potency and follow through will be questionable. Alternatively, should there be an innate shift in sentiment, the greenback can quickly return to its role as the market’s preferred reserve currency – for better or worse – and pitch into a serious trend.Looking at the backdrop for capital markets beyond S&P 500’s record highs, conditions looks highly suspect. This past week, volume on the S&P 500 was the lowest seen on a non-holiday period since the markets were closed after the September 2001 terrorist attacks in New York – an extension of a steady trend. Leverage used at the NYSE has moved to record highs. Exposure to exceptionally risky assets has grown. Retail interest in riskier assets has ramped up while ‘professional’ exposure has fled at the fastest pace in years. Meanwhile, volatility indicators show extreme complacency while rates of return are near record lows… - JKWritten by: John Kicklighter, Chief StrategistSign up for John’s email distribution list, here.original source

Dollar Could Put in for a Natural Rebound or Explosive RallyFundamental Forecast for US Dollar: BullishA range of Fed officials stay out of the way of the September Taper timetable US Treasury auctions show a slow rebound in foreign interest, but total demand weakening A strong showing in US service sector activity and trade reinforces growth, Taper outlook Over the past week, the Dow Jones FXCM Dollar Index (ticker = USDollar) suffered its worst weekly decline since December 2011 and its longest string of daily losses since December 2010. Taken without context, that is a strong bearish sign. However, when we consider the fundamental and technical backdrop; this situation looks like a launching point for a dollar rally. The question is whether it will be a mild, natural correction or an explosive rally with genuine trend generation. That outcome will be determined by the progress found on the market’s primary fundamental concerns: the market’s appetite for risk and speculation surrounding the Fed’s ‘Taper’.To understand where the dollar will move heading forward, we have to establish the conditions under which it has arrived at its current position. The slide through this past week was extraordinary for both its consistency and intensity. Yet, the slide evolved without the burden of the benchmark currency’s primary fundamental themes. Looking for evidence of a rebound in risk appetite; the speculative-favorite S&P 500 meandered – trading on the lowest non-holiday volume since the September 2011 terrorist attack – while other measures of sentiment similarly floundered. As for Taper premiums, both speeches by Fed officials’ speeches and data on the eco! nomic docket reinforced the probability of a September move by the central bank.Without conviction, the kind of move that we have seen this past week would more appropriately be labeled a ‘natural correction’. Though, traders know that such moves are temporary in nature without a strong shift in conviction and participation to change the underlying current. A simple look at market momentum, we find both the 100 and 200-day simple moving averages are below spot and rising steadily. So long as the systemic conditions behind the capital markets and investor sentiment don’t change, a return to trend for the greenback grows more likely with each day. Yet, the force of that transition depends on the accelerants available to facilitate it.The first thing we have to notice, is that the economic docket does not carry the kind of event risk that we would expect to definitively wipe out risk trends nor verify the September time frame for the Fed’s first reduction in its stimulus program. It is difficult to determine what known event risk short of the next FOMC rate decision (on September 18th) can carry enough influence to upset the current equilibrium. This past week, remarkably strong numbers for US trade and service-sector activity reinforced the more dubious – but positive – 2Q GDP and employment figures from the previous week. Furthermore, the Fed speeches from the period – particularly extreme dove Charles Evans – were clearly shaped to avoid contradicting expectations of a September start for the stimulus wind down. Yet, despite this combination, confidence in stimulus-backed speculative-position held fast. In the week ahead, we have another round of contributory data to the stimulus debate as well as central bank talks on tap; but these listings don’t seem to be any more convincing than what we have recently priced in. On Tuesday, non-voting Atlanta Fed President Dennis Lockhart (a hawk on QE) will speak on the economy, while voter St. Louis Fed Preside! nt James ! Bullard (a QE dove) is set to speak on monetary policy on Wednesday and the economy Thursday. For data, retail sales, the consumer price index and University of Michigan consumer sentiment survey are all notable.If this list of indicators and speeches can’t generate an explicit shift in risk trends, the natural ebb and flow will guide the dollar. Given the hefty move by the benchmark currency this past week despite the lack of drive, a rebound is likely. Yet, its potency and follow through will be questionable. Alternatively, should there be an innate shift in sentiment, the greenback can quickly return to its role as the market’s preferred reserve currency – for better or worse – and pitch into a serious trend.Looking at the backdrop for capital markets beyond S&P 500’s record highs, conditions looks highly suspect. This past week, volume on the S&P 500 was the lowest seen on a non-holiday period since the markets were closed after the September 2001 terrorist attacks in New York – an extension of a steady trend. Leverage used at the NYSE has moved to record highs. Exposure to exceptionally risky assets has grown. Retail interest in riskier assets has ramped up while ‘professional’ exposure has fled at the fastest pace in years. Meanwhile, volatility indicators show extreme complacency while rates of return are near record lows… - JKWritten by: John Kicklighter, Chief StrategistSign up for John’s email distribution list, here.original source

Tuesday, April 28, 2015

Dollar Could Put in for a Natural Rebound or Explosive Rally

Dollar Could Put in for a Natural Rebound or Explosive RallyFundamental Forecast for US Dollar: BullishA range of Fed officials stay out of the way of the September Taper timetable US Treasury auctions show a slow rebound in foreign interest, but total demand weakening A strong showing in US service sector activity and trade reinforces growth, Taper outlook Over the past week, the Dow Jones FXCM Dollar Index (ticker = USDollar) suffered its worst weekly decline since December 2011 and its longest string of daily losses since December 2010. Taken without context, that is a strong bearish sign. However, when we consider the fundamental and technical backdrop; this situation looks like a launching point for a dollar rally. The question is whether it will be a mild, natural correction or an explosive rally with genuine trend generation. That outcome will be determined by the progress found on the market’s primary fundamental concerns: the market’s appetite for risk and speculation surrounding the Fed’s ‘Taper’.To understand where the dollar will move heading forward, we have to establish the conditions under which it has arrived at its current position. The slide through this past week was extraordinary for both its consistency and intensity. Yet, the slide evolved without the burden of the benchmark currency’s primary fundamental themes. Looking for evidence of a rebound in risk appetite; the speculative-favorite S&P 500 meandered – trading on the lowest non-holiday volume since the September 2011 terrorist attack – while other measures of sentiment similarly floundered. As for Taper premiums, both speeches by Fed officials’ speeches and data on the eco! nomic docket reinforced the probability of a September move by the central bank.Without conviction, the kind of move that we have seen this past week would more appropriately be labeled a ‘natural correction’. Though, traders know that such moves are temporary in nature without a strong shift in conviction and participation to change the underlying current. A simple look at market momentum, we find both the 100 and 200-day simple moving averages are below spot and rising steadily. So long as the systemic conditions behind the capital markets and investor sentiment don’t change, a return to trend for the greenback grows more likely with each day. Yet, the force of that transition depends on the accelerants available to facilitate it.The first thing we have to notice, is that the economic docket does not carry the kind of event risk that we would expect to definitively wipe out risk trends nor verify the September time frame for the Fed’s first reduction in its stimulus program. It is difficult to determine what known event risk short of the next FOMC rate decision (on September 18th) can carry enough influence to upset the current equilibrium. This past week, remarkably strong numbers for US trade and service-sector activity reinforced the more dubious – but positive – 2Q GDP and employment figures from the previous week. Furthermore, the Fed speeches from the period – particularly extreme dove Charles Evans – were clearly shaped to avoid contradicting expectations of a September start for the stimulus wind down. Yet, despite this combination, confidence in stimulus-backed speculative-position held fast. In the week ahead, we have another round of contributory data to the stimulus debate as well as central bank talks on tap; but these listings don’t seem to be any more convincing than what we have recently priced in. On Tuesday, non-voting Atlanta Fed President Dennis Lockhart (a hawk on QE) will speak on the economy, while voter St. Louis Fed Preside! nt James ! Bullard (a QE dove) is set to speak on monetary policy on Wednesday and the economy Thursday. For data, retail sales, the consumer price index and University of Michigan consumer sentiment survey are all notable.If this list of indicators and speeches can’t generate an explicit shift in risk trends, the natural ebb and flow will guide the dollar. Given the hefty move by the benchmark currency this past week despite the lack of drive, a rebound is likely. Yet, its potency and follow through will be questionable. Alternatively, should there be an innate shift in sentiment, the greenback can quickly return to its role as the market’s preferred reserve currency – for better or worse – and pitch into a serious trend.Looking at the backdrop for capital markets beyond S&P 500’s record highs, conditions looks highly suspect. This past week, volume on the S&P 500 was the lowest seen on a non-holiday period since the markets were closed after the September 2001 terrorist attacks in New York – an extension of a steady trend. Leverage used at the NYSE has moved to record highs. Exposure to exceptionally risky assets has grown. Retail interest in riskier assets has ramped up while ‘professional’ exposure has fled at the fastest pace in years. Meanwhile, volatility indicators show extreme complacency while rates of return are near record lows… - JKWritten by: John Kicklighter, Chief StrategistSign up for John’s email distribution list, here.original source

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment